Step 1: Learn the basics

Understand the moving pieces before you try to solve everything at once.

Joe Pine Realtors First-Time Homebuyer Workbook

A clear, client-facing workbook built specifically for Rhode Island and Massachusetts first-time homebuyers

Joe Pine Realtors | Platinum Real Estate Group at Keller Williams Leading Edge

On-time payments matter most. Late payments usually matter more than buyers expect.

High revolving balances can put pressure on both your score and your monthly budget.

Some items carry more weight than others, but unresolved issues should never be ignored.

How much of your available credit you are using can matter almost as much as the balance itself.

Incorrect balances, duplicate accounts, or outdated information can hold you back for no good reason.

“Not perfect” does not always mean “not possible.” Some buyers need cleanup. Some need the right loan path. Some simply need to see their full picture before deciding what to do next.

When you can see the details clearly, you can decide what actually needs attention and what may already be workable.

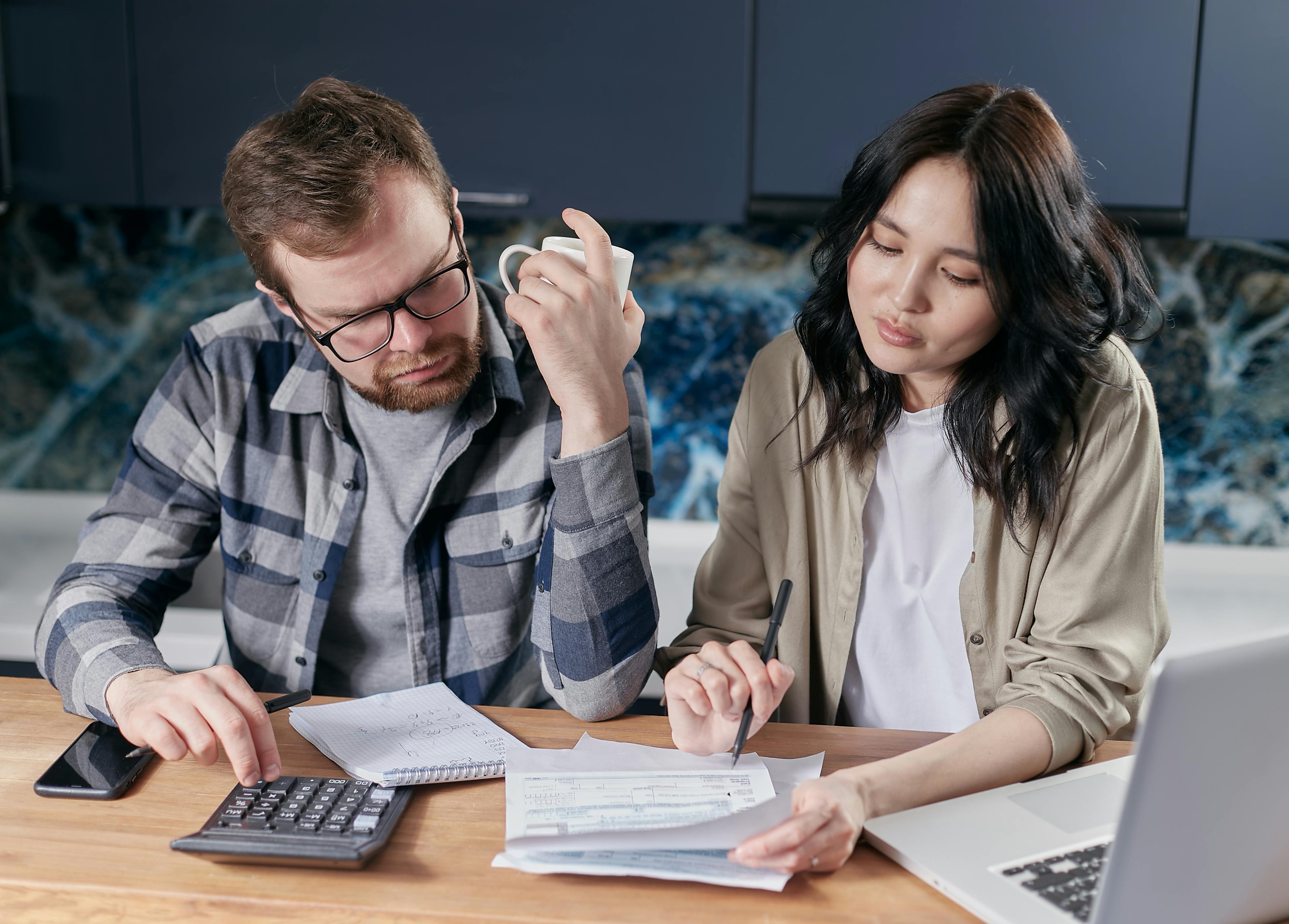

DTI can vary by loan type, lender, underwriting findings, reserves, score, compensating factors, and the strength of the full file. That is why preapproval looks at the full picture, not just one number.

DTI is really a budgeting snapshot: what must go out each month compared with what comes in.

Every required payment you remove can help in two ways: it may strengthen how your file looks to a lender, and it may also make your future monthly budget feel better after you buy.

Cleaning up avoidable payments can make the numbers look better on paper and feel better in real life.

A maximum approval number is not a recommendation. It is just a ceiling.

Your payment should still leave room for groceries, gas, savings, travel, gifts, and real life expenses.

Ask yourself how the number would feel if one surprise bill landed next month.

“Would this still feel okay on a normal Tuesday night?” That answer usually matters more than what looks possible on paper.

The right payment should support your life after closing, not just help you get to the closing table.

Separating must-haves, nice-to-haves, and true deal-breakers makes the search more focused and less emotional.

When your payment target and priorities are clear, the right homes tend to stand out much faster.

It helps you better understand the condition of the property and where you may want more information before moving forward.

The purpose is not to scare you out of buying. It is to help you understand what you are buying and decide how you want to proceed.

Inspecting the home gives you clearer facts, better questions, and a stronger decision-making position.